Sorting through roof replacement insurance coverage can feel overwhelming for Central Florida homeowners facing storm damage or the effects of an aging roof. With complex policy language and region-specific requirements, understanding what is truly covered means more than a quick scan of your documents. This article helps clarify insurance policy details and exposes common misconceptions, equipping you to make informed choices about coverage, claims, and renovation decisions.

Table of Contents

- Roof Replacement Coverage Defined And Debunked

- Types Of Roof Replacement Insurance Policies

- How Roof Replacement Claims Process Works

- Coverage Limits, Exclusions, And Fine Print

- Costs, Deductibles, And Out-Of-Pocket Factors

- Common Coverage Mistakes Central Floridians Make

Key Takeaways

| Point | Details |

|---|---|

| Understand Policy Types | Familiarize yourself with the distinctions between Actual Cash Value, Replacement Cost Value, and Extended Replacement Cost policies to choose the best coverage for your needs. |

| Maintain Documentation | Keep meticulous records of maintenance, inspections, and damage to support your insurance claims and ensure eligibility for coverage. |

| Evaluate Coverage Limits | Be aware of exclusions related to wear and tear, roof age depreciation, and specific damage limitations to avoid surprises during claims processing. |

| Plan for Out-of-Pocket Costs | Consider factors such as deductibles and additional expenses when budgeting for roof replacement to manage financial responsibilities effectively. |

Roof Replacement Coverage Defined and Debunked

Homeowners in Central Florida face unique challenges when understanding roof replacement insurance coverage. Insurance policies are complex documents filled with technical language that can confuse even savvy property owners. Identifying false claims about coverage requires careful examination of the details within your specific policy.

Roof replacement coverage isn’t universal and varies dramatically based on several critical factors:

- Age of your roof

- Type of existing roofing material

- Cause of damage (weather-related vs. general wear)

- Specific insurance policy provisions

- Local building code requirements

Most homeowner insurance policies provide partial coverage for roof damage, but rarely offer full replacement without specific conditions. Typically, insurers will evaluate roof damage through a depreciation model, which means older roofs receive reduced compensation. This means a 15-year-old roof might only get 50% of replacement costs compared to a newer roof.

Insurance providers in Central Florida often have specialized provisions related to hurricane and storm damage, which can significantly impact roof replacement coverage. Roof replacement in Central Florida requires understanding these nuanced regional considerations, especially given the area’s vulnerability to extreme weather events.

Pro tip: Always photograph roof damage immediately after an incident and document everything meticulously to support your insurance claim.

Types of Roof Replacement Insurance Policies

Central Florida homeowners must understand the nuanced landscape of insurance policies covering roof replacement. Insurance industry snapshots reveal multiple coverage types that can significantly impact your roof replacement strategy.

Homeowners typically encounter three primary types of roof replacement insurance policies:

-

Actual Cash Value (ACV) Policies

- Reimburses roof’s current market value

- Factors in depreciation

- Lowest cost monthly premium

-

Replacement Cost Value (RCV) Policies

- Covers full roof replacement cost

- No depreciation subtraction

- Higher monthly premiums

-

Extended Replacement Cost Policies

- Provides additional coverage beyond standard limits

- Protects against unexpected construction cost increases

- Best for areas with volatile construction markets

In Central Florida, hurricane and storm damage considerations make Replacement Cost Value policies particularly attractive. These policies provide more comprehensive protection, acknowledging the region’s unique weather challenges. Roof replacement scenarios demonstrate how different policy types respond to various damage circumstances.

Insurance providers often incorporate specific clauses related to roof age, material type, and maintenance history. Older roofs or those with pre-existing damage might face more restrictive coverage options, making proactive maintenance crucial for homeowners.

Pro tip: Schedule an annual professional roof inspection to maintain your insurance eligibility and document your roof’s ongoing condition.

Here’s how the main roof replacement policy types compare for Central Florida homeowners:

| Policy Type | Depreciation Applied | Upfront Premium Cost | Best for Weather Risks |

|---|---|---|---|

| Actual Cash Value (ACV) | Yes, value decreases by age | Lowest | Minimal protection; budget priorities |

| Replacement Cost Value (RCV) | No, pays full replacement | Higher | Strong storm and hurricane coverage |

| Extended Replacement Cost | Extra coverage over policy | Highest | Unpredictable construction costs |

How Roof Replacement Claims Process Works

Navigating a roof replacement insurance claim in Central Florida requires strategic planning and meticulous documentation. Filing home insurance claims involves several critical steps that can significantly impact your potential settlement.

The roof replacement claims process typically follows these essential stages:

-

Initial Damage Assessment

- Document all roof damage with clear, dated photographs

- Measure and record specific areas of destruction

- Avoid making permanent repairs before insurance inspection

-

Insurance Notification

- Contact your insurance provider immediately

- Provide comprehensive damage documentation

- Request an official claims adjuster visit

-

Professional Inspection

- Insurance adjuster evaluates roof damage

- Compares findings with your initial documentation

- Determines coverage eligibility

Florida property damage guidance emphasizes the importance of understanding your specific policy’s nuances before and during the claims process. Central Florida homeowners should recognize that hurricane and storm damage claims follow unique protocols compared to standard wear-and-tear scenarios.

Insurance providers will typically require extensive evidence demonstrating that the roof damage resulted from covered events. Maintenance records, photographic evidence, and professional inspection reports become crucial in substantiating your claim and maximizing potential reimbursement.

Pro tip: Create a dedicated digital folder storing all roof-related documents, including maintenance records, inspection reports, and damage photographs, to streamline your claims process.

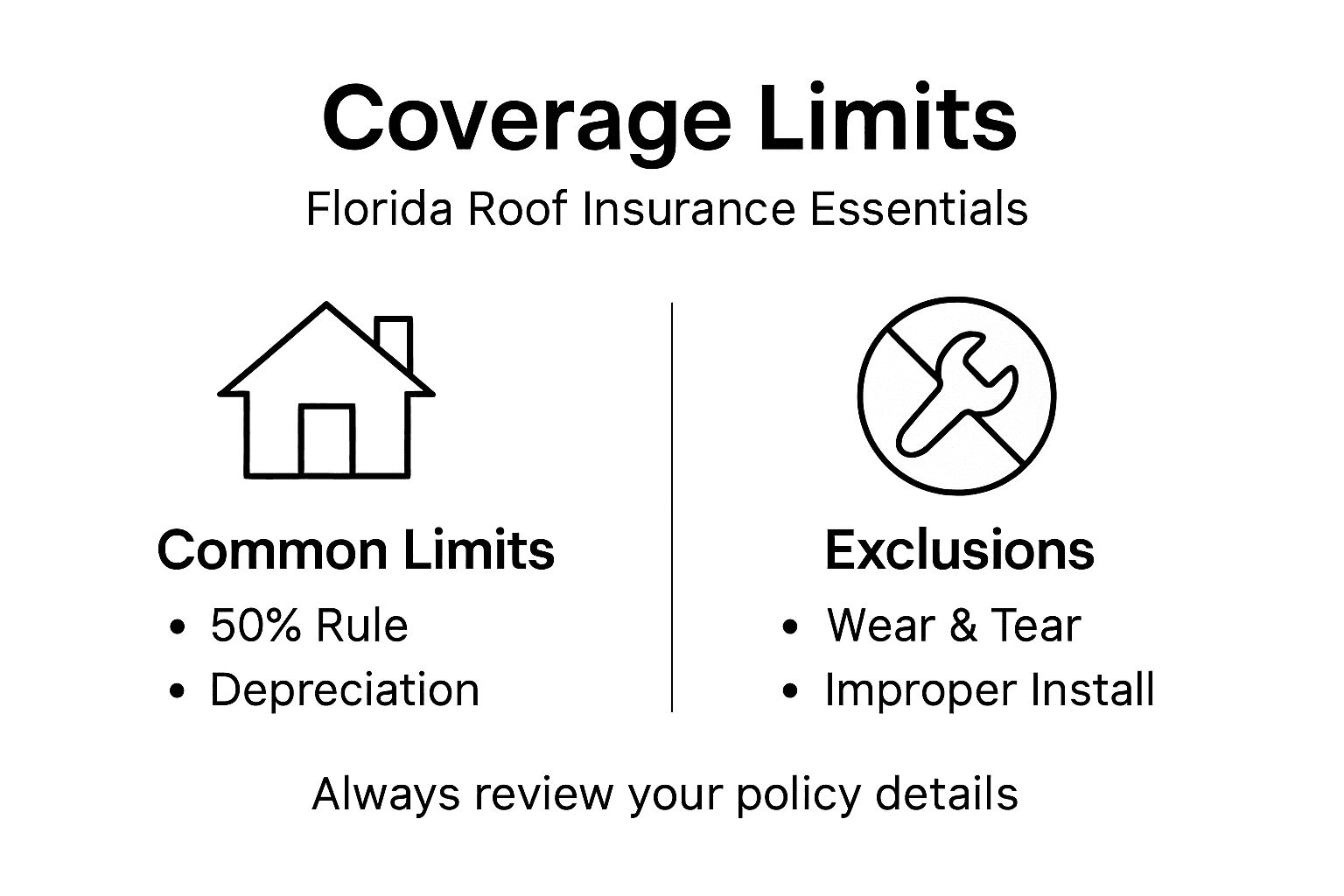

Coverage Limits, Exclusions, and Fine Print

Understanding the intricate details of roof replacement insurance requires careful examination of policy language and limitations. Repair versus replacement decisions reveal critical thresholds that significantly impact homeowner coverage in Central Florida.

Most insurance policies contain several key exclusions that homeowners must understand:

-

Standard Wear and Tear

- Typically NOT covered by insurance

- Gradual deterioration considered homeowner responsibility

- Maintenance records become crucial evidence

-

Age-Related Depreciation

- Roof over 15 years may receive reduced compensation

- Actual Cash Value policies factor in significant depreciation

- Replacement Cost Value policies offer more comprehensive coverage

-

Specific Damage Limitations

- Hurricane damage might have separate deductibles

- Wind-related damages have unique claim requirements

- Cosmetic versus structural damage distinctions matter

Roof guide standards emphasize the importance of understanding building code compliance in insurance claims. Central Florida homeowners should recognize that insurance providers often require roofs to meet specific regional construction standards to qualify for full coverage.

The 50 percent rule becomes critical in many policies. If repair costs exceed 50 percent of full replacement value, insurers may mandate complete roof replacement. This nuanced provision can dramatically impact your claim’s outcome and potential financial recovery.

Pro tip: Request a comprehensive policy review annually to understand evolving coverage limits and potential exclusions specific to your roof’s age and condition.

Costs, Deductibles, and Out-of-Pocket Factors

Navigating roof replacement expenses requires a strategic understanding of insurance financial structures. Insurance premium considerations reveal complex relationships between deductibles, coverage, and homeowner financial responsibilities in Central Florida.

Homeowners typically encounter several critical out-of-pocket cost factors:

-

Deductible Structures

- Hurricane deductibles often differ from standard claims

- Percentage-based vs. fixed dollar amount deductibles

- Can range from $500 to 5% of home’s insured value

-

Premium Impact Factors

- Higher deductibles lower monthly insurance costs

- Roof age and condition directly influence premiums

- Credit score and claims history affect pricing

-

Potential Additional Expenses

- Temporary housing during roof replacement

- Upgrades beyond standard insurance coverage

- Permit and inspection fees

Deductible management strategies demonstrate that homeowners can strategically balance out-of-pocket expenses with long-term financial protection. Central Florida residents must carefully evaluate their financial capacity when selecting insurance deductible levels.

Most roof replacement scenarios involve complex financial calculations. The total cost of ownership extends beyond immediate repair expenses, incorporating potential future maintenance, insurance premiums, and potential property value impacts.

Pro tip: Calculate your maximum potential out-of-pocket expenses by comparing multiple insurance policies and understanding their specific deductible structures.

Consider these critical insurance cost influences when planning a roof replacement budget:

| Cost Factor | Central Florida Impact | Typical Range |

|---|---|---|

| Hurricane Deductible | Can greatly exceed standard | 2% – 5% of insured value |

| Roof Age Surcharge | Older roofs increase premium | $100-$400/year extra |

| Temporary Housing | Needed during major replacements | $500-$2,000 per claim |

Common Coverage Mistakes Central Floridians Make

Roof replacement insurance in Central Florida is fraught with potential pitfalls that can dramatically impact homeowners’ financial protection. Florida Building Code requirements highlight critical nuances that many homeowners unknowingly overlook.

The most common coverage mistakes include:

-

Maintenance Documentation Neglect

- Failing to maintain detailed repair records

- Skipping annual professional roof inspections

- Not photographing damage immediately

-

Policy Misunderstanding

- Assuming all storm damage is automatically covered

- Not understanding hurricane deductible specifics

- Overlooking roof age depreciation clauses

-

Code Compliance Ignorance

- Unaware of new roofing material requirements

- Not meeting updated building code standards

- Assuming older installation methods remain valid

Roof repair assistance guidelines reveal that documentation and proactive maintenance are crucial for successful insurance claims. Central Florida’s unique weather conditions demand a more sophisticated approach to roof replacement coverage.

Insurance providers scrutinize every detail, making precise documentation and ongoing maintenance critical. Homeowners who fail to understand these nuanced requirements risk significant financial exposure during roof replacement scenarios.

Pro tip: Create a digital portfolio documenting your roof’s maintenance history, including photographs, professional inspection reports, and repair records to strengthen potential insurance claims.

Protect Your Central Florida Home with Trusted Roof Replacement Experts

Understanding roof replacement coverage can be overwhelming for Central Florida homeowners facing hurricane risks and complex insurance policies. Key challenges include navigating age-related depreciation, hurricane deductibles, and specific damage documentation. You need a roofing partner who not only delivers expert craftsmanship but also understands these insurance nuances and local building codes.

At Thomas Roofing and Repair, we specialize in residential and commercial roof replacement and storm damage repair throughout Brevard, Volusia, and Orange counties. Our team helps you prepare precise damage assessments and maintain detailed maintenance records to support your insurance claim — making the roof replacement process smoother and more affordable. Enjoy peace of mind knowing your roof installation meets Florida’s stringent building standards and that you have reliable support through every step.

Ready to safeguard your home with a roof built to last and insurance-ready documentation?

Explore our expert roofing services that protect your biggest investment from unpredictable weather and insurance pitfalls.

Contact us today for a free roof inspection and estimate to ensure your next claim maximizes your coverage and minimizes out-of-pocket costs. Visit Thomas Roofing and Repair to get started now.

Frequently Asked Questions

What factors affect roof replacement insurance coverage?

Roof replacement coverage varies based on the age of the roof, type of roofing material, cause of damage, specific policy provisions, and local building code requirements.

How do different types of roof replacement insurance policies compare?

Homeowners typically encounter Actual Cash Value (ACV) policies, which factor in depreciation; Replacement Cost Value (RCV) policies, which cover full replacement costs; and Extended Replacement Cost policies, which provide additional coverage against unexpected cost increases.

What steps should I follow when filing a roof replacement insurance claim?

The claims process involves documenting damage with photographs, notifying your insurance provider, and having an insurance adjuster evaluate the damage before making any repairs.

What common mistakes should homeowners avoid regarding roof replacement insurance?

Common mistakes include neglecting maintenance documentation, misunderstanding the specifics of the insurance policy, and ignoring compliance with updated building code standards.

Recommended

- Roof Replacement in Central Florida – What Homeowners Need to Know

- Roofers Orlando FL – Thomas Roofing & Repair Inc.

- What Is Roof Replacement and Why It Matters

- Roofing Company Orlando FL – Thomas Roofing & Repair Inc.

- Quelles sont les précautions à prendre lors d’un orage en présence de foudre? – LPS Manager