TL;DR:

- Roof condition significantly impacts insurance, financing, and resale value for Central Florida investments.

- Upgrading to compliant, impact-resistant roofs can boost property value and NOI by up to 20 percent.

- Proactive roofing strategies enhance deal momentum, negotiation leverage, and long-term portfolio growth.

If you’re evaluating investment properties in Central Florida and treating the roof as a line-item afterthought, you’re leaving serious money on the table. The roof isn’t just a cap on a building. It’s a gatekeeper for financing, insurance coverage, and resale value. In a market shaped by hurricane seasons and increasingly strict insurer requirements, roofs over 15 years old can kill deals before they even reach the closing table. This guide breaks down exactly how roofing decisions shape investor outcomes across Brevard, Volusia, and Orange counties, and what you can do to make roofing work for your returns.

Table of Contents

- Why roofing is a deal-maker or deal-breaker for investors

- How roof quality drives property value and NOI

- Evaluating roofs in multifamily and commercial investments

- Smart roofing strategies for maximizing Central Florida ROI

- Perspective: What most real estate investors overlook about roofing

- Upgrade your investment with expert Central Florida roofing

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Roof age impacts deals | Older roofs can block insurance or financing, stalling property sales. |

| Quality boosts value | A high-quality roof can raise property value by up to 20 percent in Central Florida. |

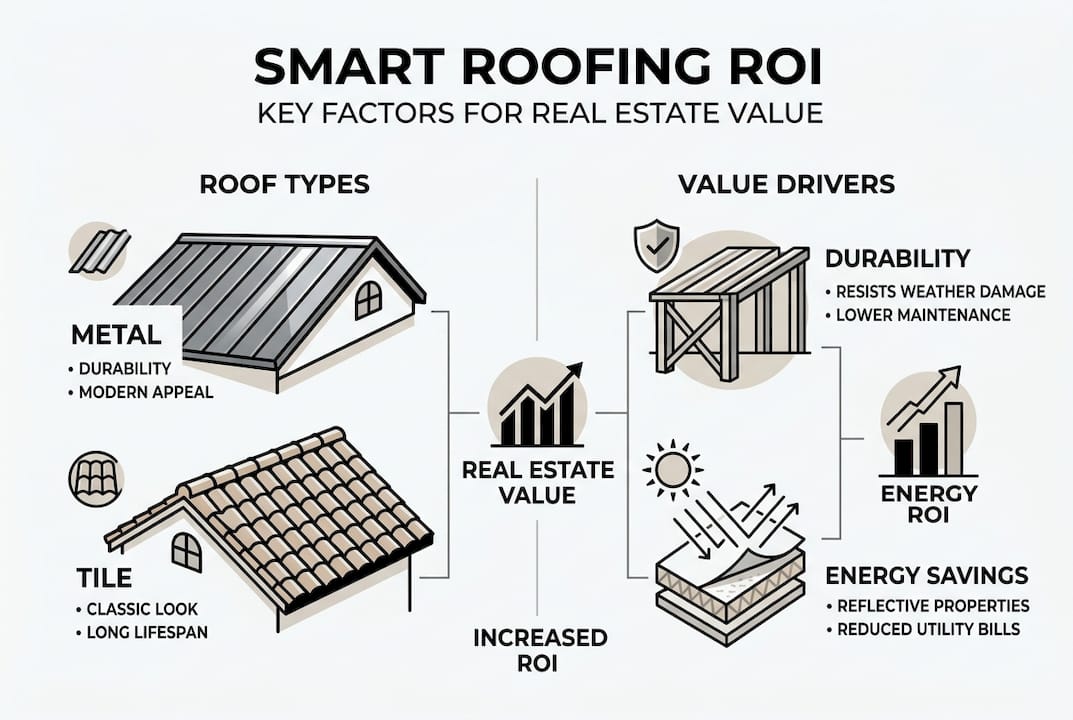

| ROI varies by material | Metal and tile roofs provide higher ROI than asphalt shingles during resale. |

| Proactive evaluation pays | Assessing and upgrading roofs before listing improves appraisals and sales outcomes. |

Why roofing is a deal-maker or deal-breaker for investors

Most investors run the numbers on location, rent potential, and cap rate. Fewer ask the one question that can derail all of it: what’s the roof situation? In Central Florida, that question carries more weight than almost anywhere else in the country.

Lenders and insurers look at the roof before they look at almost anything else. A property with an aging or non-compliant roof can struggle to secure homeowner’s insurance, and without insurance, no conventional lender will fund the deal. The insurability risks from older roofs are especially acute here because Florida’s hurricane exposure pushes insurers to apply stricter standards than they would in low-risk states.

Here’s what that means in practice. A property with a roof that’s 16 years old might look like a great value play on paper. But when your buyer’s lender orders an inspection, or when your own insurer refuses to renew the policy, that “great value” becomes a liability fast. You’re either forced to replace the roof at negotiation time (at reduced leverage) or the deal collapses entirely.

Key deal risks tied to roof condition:

- Roofs over 15 years old commonly trigger insurance denials or non-renewals

- Non-compliant materials can fail hurricane wind rating requirements

- Failing inspection reports can trigger renegotiation or buyer walkouts

- Older roofs on commercial properties reduce appraised value

- Insurance gaps create financing voids that stall closing timelines

The comparison below shows how dramatically roof condition changes the math on a property:

| Factor | Property with aging roof | Property with compliant new roof |

|---|---|---|

| Insurance availability | Limited or denied | Standard market access |

| Lender financing | Often requires escrow or denial | Clean approval path |

| Buyer pool | Narrowed to cash buyers | Full market access |

| Negotiation leverage | Weakened | Strong |

| Sale timeline | Extended | Standard |

When you’re trying to maximize property value on an investment property, the roof is the first place to look. Our residential roofing services are built around exactly this kind of strategic thinking, not just replacing shingles but protecting your investment from the top down.

How roof quality drives property value and NOI

Once you understand the financing and insurance stakes, the next question is straightforward: how much does a quality roof actually move the needle on value and income? The numbers are more significant than most investors expect.

Quality roofing increases commercial property value by 15 to 20 percent in Central Florida, driven by better durability, stronger tenant appeal, lower insurance overhead, and energy savings. For a $1 million commercial asset, that’s a $150,000 to $200,000 swing based largely on the roof condition. That’s not a maintenance issue. That’s an asset management decision.

For residential investment properties, the story is similar. New roofs nationally recoup 50 to 70 percent of their cost in added resale value, with asphalt shingles returning roughly 60 percent and metal or tile materials coming in at 85 percent or higher. In Florida specifically, a new roof sidesteps the deal-killing inspection outcomes that plague older properties and supports stronger appraisals.

How roofing upgrades improve NOI for Central Florida investors:

- Lower insurance premiums from impact-rated and energy-efficient materials

- Reduced maintenance costs from more durable systems

- Higher tenant retention due to fewer leak-related complaints

- Stronger appraisals that support better refinancing terms

- Reduced vacancy by signaling a well-maintained property to prospective tenants

Here’s a comparison of roofing materials and their investment return profiles:

| Material | Avg. cost per sq. ft. | ROI at resale | Hurricane rating | Insurance impact |

|---|---|---|---|---|

| Asphalt shingles | $3.50 to $5.50 | ~60% | Moderate | Standard |

| Metal roofing | $7.00 to $12.00 | 85%+ | High | Often discounted |

| Concrete tile | $8.00 to $14.00 | 85%+ | High | Often discounted |

| TPO (commercial) | $5.00 to $9.00 | Variable | High | Favorable |

Understanding roofing’s effect on value goes beyond picking the right material. Timing, code compliance, and installation quality all factor in. Choosing the right Central Florida roofing materials for your property type and use case is where the real ROI lives.

Pro Tip: If you’re refinancing or selling within three years, a metal or tile roof replacement often delivers better returns than a cosmetic renovation. Appraisers and insurers weigh structural improvements more heavily than surface upgrades in this market.

Evaluating roofs in multifamily and commercial investments

Multifamily and commercial deals add complexity to the roof equation. You’re not just looking at one home. You’re looking at a system that protects multiple income-producing units, and any failure cascades across your NOI.

Evaluating multifamily roofs in Central Florida requires a focused look at age, hurricane protection capability, and drainage design. A roof with poor drainage on a 40-unit property can cause water intrusion across multiple units simultaneously, triggering repair costs, tenant complaints, and potential habitability claims all at once.

What to inspect on multifamily and commercial roofs:

- Age and material type relative to expected lifespan

- Drainage slope and condition of gutters, scuppers, and downspouts

- Evidence of prior patching or layered repairs (a sign of deferred maintenance)

- Wind uplift ratings and compliance with Florida Building Code

- Condition of penetrations around HVAC units, vents, and skylights

- Flashings and seam integrity on flat or low-slope systems

A roof in poor condition doesn’t just cost money to fix. It creates a risk discount in how buyers and lenders price the asset. Higher cap rate requirements for risky properties mean lower valuations at exit, even if your rent roll looks solid. Working with a certified roof specialist before you close gives you negotiation data and avoids expensive surprises post-acquisition.

“Investors who skip roof due diligence on multifamily assets often find themselves funding a six-figure replacement within 18 months of closing, which wipes out the first year of cash flow before they’ve had a chance to stabilize the asset.”

For commercial properties specifically, understanding key roofing mechanics for systems like TPO, EPDM, and modified bitumen is important. These flat-roof systems have different failure modes than residential pitched roofs, and they require different inspection criteria. Our commercial roof repair services are designed to address those specific needs, including post-storm assessments and warranty-backed repairs.

Pro Tip: Always request a roof certification from a licensed contractor as part of your due diligence package on any commercial or multifamily deal. It gives you a documented condition baseline and can be used as leverage in seller negotiations.

Smart roofing strategies for maximizing Central Florida ROI

Knowing the stakes is one thing. Acting on them strategically is where investors separate themselves. Here’s how to make roofing a deliberate profit lever in your Central Florida portfolio.

Actionable investment-driven roofing upgrade checklist:

- Time roof replacements six to twelve months before a planned sale or refinance to maximize appraisal impact

- Prioritize impact-resistant and hurricane-rated materials for insurance premium reductions

- Avoid trendy materials with unproven long-term performance in Florida’s climate

- Match the roof system to the property type (pitched for residential, low-slope for commercial)

- Confirm all work meets Florida Building Code and local permitting requirements

- Get a post-installation warranty and transfer it to buyers as a selling point

- Budget for regular inspections after storm seasons to catch minor issues before they compound

Metal and tile roofs consistently deliver 85% or better ROI at resale in Florida, making them a strong choice for properties where you’re planning a three to five year hold and exit. Asphalt shingles are a lower upfront cost and still deliver solid returns in the right context, particularly for shorter-hold or rental-focused strategies.

Energy efficiency is another underrated angle. Impact-resistant roofing qualifies for insurance discounts under Florida’s wind mitigation program, which can meaningfully reduce annual carrying costs across a portfolio. The savings compound over a hold period and make a real difference at exit when buyers factor in operating costs.

Be cautious about green vs. code-compliant roofing trade-offs. Green roofs have sustainability appeal but can carry higher lifecycle costs that don’t pencil out in the Florida market. Code-compliant, impact-rated systems typically deliver better risk-adjusted returns here. Always model the total cost of ownership, not just the upfront installation price.

Choosing the best roofing materials for your specific property is a decision that deserves the same rigor you’d apply to financing structure or tenant selection. A local expert who understands Brevard, Volusia, and Orange county building codes is worth far more than a general contractor who treats Florida like any other state.

Perspective: What most real estate investors overlook about roofing

Here’s something we’ve seen play out repeatedly in Central Florida deals: investors who know their numbers cold will still take a shortcut on the roof because it feels like a cost, not a strategy.

Conventional wisdom says to minimize renovation spend and maximize cash-on-cash return as fast as possible. In most markets, that logic holds. In a hurricane-exposed market where insurers pull coverage and lenders flinch at old roofs, cutting corners on the roof is one of the most expensive decisions an investor can make.

The savvy investors we work with treat the roof as a strategic asset from day one. They ask about roof age before they ask about rent rolls. They budget for compliant upgrades before acquisition, not as a reactive fix after a failed inspection. That shift in mindset, from maintenance to long-term value strategy, is what separates investors who build portfolio equity efficiently from those who keep reacting to problems they could have prevented.

Proactive roofing decisions don’t just protect you from loss. They create deal momentum, improve financing terms, and generate real negotiating leverage. That’s not maintenance thinking. That’s investment thinking.

Upgrade your investment with expert Central Florida roofing

If you’re ready to turn roofing from a hassle into a profit driver, here’s how to take the next step.

At Thomas Roofing and Repair, we work with investors, property managers, and owners across Brevard, Volusia, and Orange counties who need more than just shingles replaced. They need a roofing partner who understands what’s at stake in this market. Whether you’re protecting an existing asset, preparing for a sale, or evaluating a new acquisition, our team brings the local expertise to help you choose the right system at the right time. From our storm damage repair guide to durable roof craftsmanship built for Florida conditions, we have the resources to support your strategy. Ready to get started? Explore our professional roof replacement options and request your free estimate today.

Frequently asked questions

How does roof age affect insurance and financing in Central Florida?

Most insurers in Central Florida won’t cover roofs over 15 years old, which blocks conventional financing and can halt a sale until a compliant roof is installed.

What’s the average ROI on a new roof for investment properties?

Investors typically see 50 to 85 percent ROI at resale, with metal and tile roofs delivering the highest returns, particularly in Florida’s hurricane-rated market.

How do I evaluate a roof’s condition on an investment property?

Focus on age, drainage performance, material compliance with hurricane codes, and any signs of deferred maintenance. A professional multifamily roof evaluation should also assess how condition affects your cap rate and NOI.

Are green roofs a smart investment in Central Florida?

Green roofs can carry higher lifecycle costs that don’t always pencil out here. Code-compliant, impact-rated systems typically offer better risk-adjusted returns for Central Florida investors.