TL;DR:

- A new roof can boost property value by 50 to 70% of replacement costs.

- Roof age over 15 years often causes insurance issues and reduces appraisal value.

- Proper documentation and proactive upgrades strengthen negotiation power and speed up sales.

Your roof is one of the biggest financial levers you have as a property owner in Central Florida, yet most people treat it as an afterthought until something goes wrong. A new roof boosts property value by 50 to 70% ROI and can accelerate your sale timeline significantly. Ignore it, and you risk appraisal deductions, insurance denials, and buyers walking away or demanding steep price concessions. This guide breaks down exactly how roofing decisions affect your property’s worth, your insurance eligibility, and your negotiating power, so you can make smarter choices whether you’re selling, managing rentals, or building long-term equity.

Table of Contents

- How roof condition shapes appraisal and resale value

- Insurance and roofing: The critical age thresholds

- Roofing materials and maintenance: Strategic choices for maximum value

- Leveraging roofing for higher offers and faster sales

- Why smart roofing strategy beats reactive repairs

- Unlock property value with Central Florida roofing solutions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Roof age impacts value | Older roofs lead to lower appraisals, tougher insurance, and buyer price negotiations. |

| Insurance drives decisions | Florida insurers impose strict roof age limits that can affect coverage and premiums. |

| Maintenance maximizes ROI | Documented roof care and timely upgrades offer the best path to higher offers and faster sales. |

| Material choice matters | Selecting durable, attractive roofing materials enhances curb appeal and buyer confidence. |

| Documentation is leverage | Providing warranties and inspection records can solidify deals and support property value. |

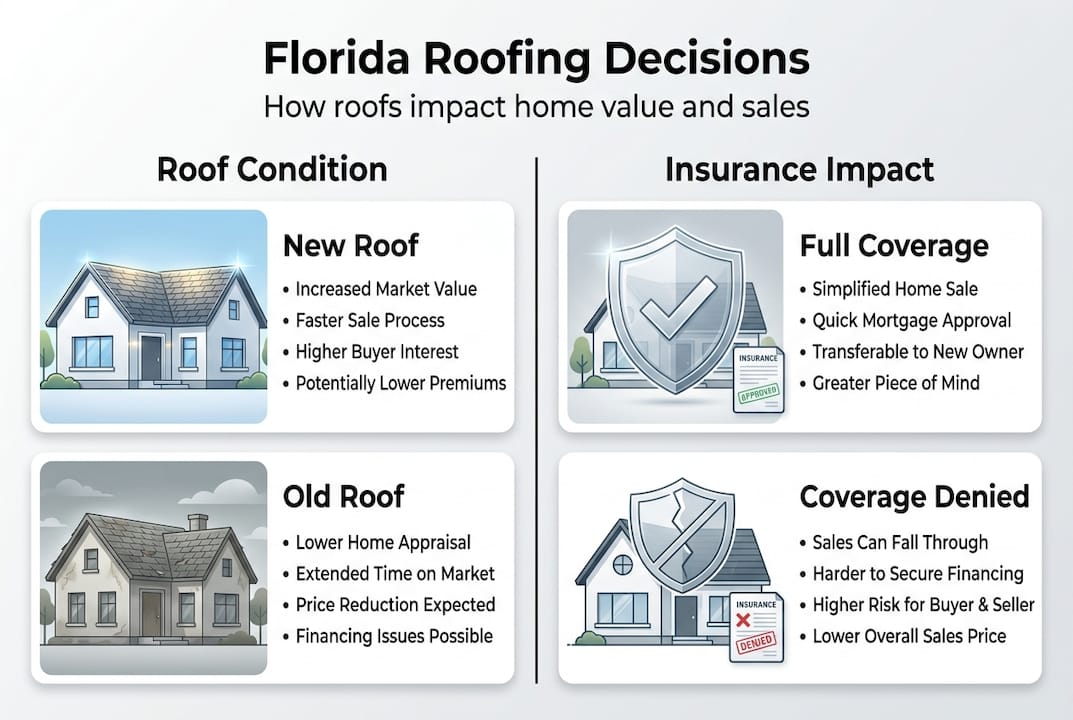

How roof condition shapes appraisal and resale value

Understanding property value starts with the roof’s condition. When an appraiser walks your property, the roof is one of the first things they assess. Age, visible wear, missing shingles, staining, and any sign of leaks all factor into the final number. Poor roof condition reduces appraisals by 5 to 10%, which on a $400,000 home means losing $20,000 to $40,000 in appraised value before negotiations even begin.

Buyers are equally unforgiving. When a home inspector flags roof issues, buyers typically request price concessions, repair credits, or they walk entirely. A roof that’s clearly aging gives buyers a reason to lowball. A new or recently serviced roof removes that leverage from the buyer’s hands and puts it back in yours.

Both cosmetic and structural roof updates matter here. Cosmetic improvements like new shingles in a complementary color or clean ridge lines boost curb appeal and first impressions. Structural updates like replacing decking, fixing flashing, or resealing valleys address the concerns appraisers and inspectors actually flag. The advantages of roof replacement go beyond aesthetics; they directly support a stronger appraisal number.

“A new roof improves curb appeal and buyer confidence, recouping 50 to 70% of replacement costs in added value.”

Here’s a quick comparison of how roof condition translates to real dollars at closing:

| Roof condition | Appraisal impact | Buyer negotiation risk | Insurance eligibility |

|---|---|---|---|

| New (0 to 5 years) | Positive, supports full value | Very low | Fully insurable |

| Good (6 to 14 years) | Neutral to slight positive | Low | Insurable with documentation |

| Aging (15 to 19 years) | Slight deduction possible | Moderate | Inspection required |

| Old (20+ years) | 5 to 10% deduction likely | High | Often denied or limited |

If you’re preparing to sell, consider a pre-listing appraisal to understand exactly where your roof stands before buyers do. Knowing your number early gives you time to act strategically. Material also plays a role in perceived value. Understanding tile roof pros and cons for Florida’s climate can help you choose upgrades that appraisers and buyers in Central Florida actually reward.

Key takeaways for appraisal impact:

- Visible damage and age are the top two roof-related appraisal deductions

- New roofing materials signal quality and reduce buyer objections

- Curb appeal from a clean, uniform roof surface supports faster offers

- Documented roof history strengthens your position with appraisers

Insurance and roofing: The critical age thresholds

Appraisal isn’t the only factor. Insurance barriers often surprise sellers and buyers alike in Florida. The state’s insurance market is one of the most scrutinized in the country, and roof age is a primary trigger for coverage issues.

Here’s how Florida insurers typically treat roof age in 2026:

| Roof age | Insurance outcome |

|---|---|

| Under 15 years | Generally insurable, standard premiums |

| 15 to 19 years | Inspection required before coverage approval |

| 20+ years | Often denied, non-renewed, or limited to ACV (actual cash value) |

Actual cash value coverage is a significant downgrade from replacement cost coverage. It means your insurer pays out what your old roof is worth today, not what it costs to replace it. For a roof that’s 22 years old, that payout could be a fraction of actual repair costs. Roof age impacts insurance eligibility and premiums in ways that directly affect your property’s marketability.

When a buyer’s insurance company refuses to cover a home because of an old roof, the deal can fall apart entirely. This is especially common in Brevard, Volusia, and Orange counties, where storm exposure adds another layer of insurer caution. Understanding the full picture through a solid roofing insurance guide is essential before you list or purchase.

Pro Tip: Replace your roof before listing if it’s approaching 15 years old. The upfront cost is often offset by the premium you can command, the insurance hurdles you eliminate, and the negotiating power you gain. A roof inspection process completed before listing also gives you documentation that reassures buyers and their lenders.

Steps to protect your insurance position as a seller or investor:

- Know your roof’s exact installation date and material type

- Schedule a professional inspection if the roof is 12 years or older

- Obtain and retain transferable roof warranties for any new or repaired work

- Address any inspection findings before listing to avoid buyer-side insurance objections

- Disclose roof age and condition accurately to avoid post-sale liability

Being proactive here isn’t just good practice. It’s a financial decision. Preparing for your home appraisal with a solid roof in place removes one of the most common deal-breakers in Florida real estate.

Roofing materials and maintenance: Strategic choices for maximum value

Roof age and insurance are only part of the equation. Ongoing care and material selection play a major role in long-term property value. The material you choose affects curb appeal, durability, insurance eligibility, and how buyers perceive the home’s overall quality.

In Central Florida, the most common residential roofing materials are asphalt shingles, tile (clay or concrete), and metal. Each has trade-offs:

- Asphalt shingles: Most affordable upfront, widely accepted by insurers, but shorter lifespan (15 to 25 years depending on quality)

- Tile roofing: Higher upfront cost, exceptional durability (40 to 50 years), strong curb appeal in Florida’s architectural styles, and favorable insurance treatment when properly maintained

- Metal roofing: Excellent wind resistance, long lifespan, growing popularity with insurers for storm-prone areas

For property managers and real estate investors, maintenance plans are essential for multifamily and investment properties. A single neglected roof across a rental portfolio can trigger cascading insurance issues, tenant complaints, and expensive emergency repairs.

Regular maintenance, meaning biannual inspections, gutter cleaning, moss or algae treatment, and prompt minor repairs, preserves the roof’s rated lifespan and keeps your documentation current. Buyers and appraisers respond well to a property that shows a consistent maintenance record. Our roof maintenance guide walks through the specific tasks that protect your investment year over year.

Pro Tip: For multifamily property managers, schedule roof inspections after every major storm season. Central Florida’s hurricane exposure means small issues become large ones fast. The roof inspection benefits for rental properties go beyond compliance; they protect your NOI (net operating income, the income left after operating expenses).

Key documentation to keep on file:

- Original installation date and contractor information

- Material specifications and warranty certificates

- All inspection reports with photos

- Records of any repairs, including scope and cost

- Insurance correspondence related to the roof

For investors weighing material upgrades, reviewing tile roof insights specific to Florida’s climate helps you match material choice to long-term ROI rather than just upfront cost.

Leveraging roofing for higher offers and faster sales

For maximum value in practice, sellers and managers should actively leverage roofing documentation. Most sellers leave money on the table simply because they don’t present their roof’s condition clearly. Buyers assume the worst when information is missing.

Even roofs in good condition but older can face insurance hurdles and slow sales in competitive markets. The solution is documentation and proactive communication, not just hoping buyers won’t notice.

“In Central Florida’s insurance-driven market, a documented roof history is as valuable as the roof itself.”

Steps to use roofing as a negotiation asset:

- Include roof age, material, and warranty status in your listing description

- Attach inspection reports and maintenance records to your seller’s disclosure

- Highlight any transferable warranties in marketing materials

- Schedule a pre-sale inspection through inspection benefits for sellers to get ahead of buyer objections

- Price your home to reflect the roof’s condition, not just square footage and location

Buyers working with lenders are often required to have roofs inspected before closing. When you already have a clean inspection on file, you remove a potential delay from the transaction. Familiarizing yourself with roof inspection terminology helps you communicate confidently with buyers, agents, and appraisers.

Additional ways to strengthen your position:

- Offer transferable roof warranty claims as part of the sale

- Provide before-and-after photos of any recent repairs

- Include energy efficiency data if metal or reflective roofing was installed

- Reference your roof in open house conversations to build buyer confidence

For investors using ARV appraisal methods (after repair value, meaning what a property is worth after improvements), a new roof is one of the most defensible line items you can present to justify a higher projected value.

Why smart roofing strategy beats reactive repairs

Most property owners wait for a leak, a storm, or a buyer’s inspector to force their hand. That reactive approach consistently costs more and yields less. We’ve seen it repeatedly across Central Florida: a seller who replaces a roof proactively walks away with a cleaner deal, fewer concessions, and a faster close than one who tries to negotiate around an aging roof.

The conventional wisdom is to defer big expenses until necessary. But in Florida’s insurance-driven market, a roof over 15 years old isn’t just an aging asset. It’s a liability that can unravel financing, scare off buyers, and trigger premium spikes for current owners. Treating your roof as a value asset rather than a maintenance burden changes how you make decisions about timing, materials, and documentation.

Long-term investors and property managers who build roofing into their asset management strategy consistently outperform those who don’t. Document everything: inspections, repairs, warranties, and material specs. That paper trail is worth real dollars at sale time. Our roof maintenance wisdom reflects years of working with Central Florida property owners who’ve learned this lesson firsthand.

Unlock property value with Central Florida roofing solutions

You now understand how roof condition, age, materials, and documentation directly shape your property’s value and saleability. The next step is working with a team that knows Central Florida’s specific insurance landscape, weather patterns, and buyer expectations.

At Thomas Roofing and Repair, we serve homeowners, property managers, and investors across Brevard, Volusia, and Orange counties with inspections, repairs, replacements, and installations built around your goals. Whether you’re navigating storm damage repair after a rough season, planning a roof replacement before listing, or starting fresh with expert roof installation, our team is ready to help you protect and grow your investment. Contact us today for a free estimate.

Frequently asked questions

How much does a new roof increase property value in Central Florida?

A new roof can increase property value by 50 to 70% of the replacement cost. This gain comes primarily through stronger buyer confidence, better curb appeal, and smoother appraisal outcomes in Florida’s competitive market.

What roof age triggers insurance problems in Florida?

Roofs over 15 years old typically require a formal inspection before insurers will approve coverage. Once a roof passes 20 years, many Florida insurers deny coverage outright or downgrade to actual cash value policies.

Will buyers pay more for documented roof improvements?

Yes. Documented repairs, active warranties, and recent inspection reports give buyers and their lenders confidence, which supports higher offers and reduces time on market. Documented roof history is one of the most underused negotiation tools sellers have.

Is ongoing roof maintenance important for rental properties?

Absolutely. Maintenance plans are essential for landlords and property managers because deferred roof care leads to insurance issues, tenant complaints, and expensive emergency repairs that erode property value fast.

What is the fastest way to leverage roofing for a better sale?

Replace the roof or complete a documented inspection before listing. This eliminates the two biggest deal-breakers in Florida real estate: insurance objections and buyer-side price concessions tied to roof condition.