Many Central Florida homeowners believe their standard homeowners insurance automatically covers any roof problem, from old age wear to hurricane damage. This misconception leads to shock when claims are denied or deductibles reach thousands of dollars. Understanding what roofing insurance actually covers, how deductibles work, and which damage types qualify for claims is essential for storm-prone regions like Brevard, Volusia, and Orange counties. This guide explains roofing insurance coverage basics, costs, policy types, and 2026 Florida regulations to help you protect your home and navigate claims successfully after storm damage.

Table of Contents

- Understanding Roofing Insurance Coverage In Central Florida

- Costs And Deductibles On Roofing Insurance In Central Florida

- Types Of Roofing Insurance Coverage: Acv Vs Rcv

- Navigating Florida’s 2026 Roof Insurance Regulations And Claims Tips

- Protect Your Central Florida Home With Trusted Roof Repair And Installation

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Coverage scope | Roofing insurance covers sudden storm damage like hurricanes and hail but excludes wear and tear or maintenance neglect. |

| Hurricane deductibles | Florida policies include separate hurricane deductibles typically 2-5% of your home’s insured value, creating significant out-of-pocket costs. |

| RCV vs ACV | Replacement cost value coverage pays full repair costs without depreciation, while actual cash value deducts depreciation from payouts. |

| Premium reduction | Wind mitigation features like hip roofs and impact-resistant materials can lower your insurance premiums substantially. |

| Claim success factors | Detailed documentation, timely reporting, and regular maintenance records significantly improve your chances of successful coverage. |

Understanding roofing insurance coverage in Central Florida

Roofing insurance protects your home against sudden damage from severe weather events common in Central Florida. Homeowners insurance typically covers roof leaks from covered perils like wind damage from hurricanes, but not damage from wear and tear or maintenance neglect. This distinction becomes critical when filing claims after storm season.

Your standard policy covers specific perils including wind damage, hail impact, and rain entering through storm-created roof openings. When a hurricane tears off shingles or a falling tree branch punctures your roof during a storm, your insurance should cover repairs. However, if your roof gradually deteriorated over years without proper maintenance, insurers will deny your claim even if a storm finally caused visible damage.

Flood damage requires separate flood insurance through the National Flood Insurance Program or private insurers. Many homeowners mistakenly believe their standard policy covers water damage from any source. If rising floodwaters damage your roof or interior, your homeowners policy will not pay for repairs. Only wind-driven rain entering through storm-damaged openings qualifies under standard coverage.

Proper maintenance documentation becomes your strongest defense against claim denials. Keep records of professional inspections, repairs, and preventive work. These records prove you maintained your roof properly and that damage resulted from covered perils, not neglect. A roofing guarantee from professional contractors adds credibility to your maintenance history.

Common covered perils for Central Florida roofs:

- Hurricane and tropical storm wind damage

- Hail impact and resulting shingle damage

- Falling trees or branches during storms

- Wind-driven rain through storm-damaged openings

- Lightning strikes causing direct roof damage

Pro Tip: Schedule professional roof inspections before hurricane season starts each year. These inspections identify minor issues before they become major problems and create documentation proving your roof was in good condition before storms hit.

Timely inspections also help you catch problems early when repairs cost less. Small issues like loose shingles or minor leaks quickly escalate into major damage during severe weather. Addressing these problems immediately maintains your coverage eligibility and prevents insurers from claiming pre-existing damage caused your losses.

Costs and deductibles on roofing insurance in Central Florida

Florida homeowners face insurance costs 2-3 times higher than the national average due to hurricane risks and elevated rebuild costs. Average Central Florida premiums range from $2,330 to $3,645 annually depending on your location, home age, construction type, and coverage limits. These premiums reflect the high probability of storm damage in our region.

Hurricane deductibles create the biggest financial surprise for homeowners. Unlike your standard deductible of $500 or $1,000, hurricane deductibles typically range from 1% to 5% of your home’s insured value. If your home is insured for $300,000 with a 2% hurricane deductible, you pay the first $6,000 of repairs out of pocket. A 5% deductible on the same home means $15,000 in upfront costs before insurance pays anything.

Your deductible type activates based on how the National Hurricane Center classifies the storm. When a named tropical storm or hurricane causes damage, your hurricane deductible applies instead of your standard deductible. This distinction matters because even tropical storms trigger the higher deductible, not just major hurricanes.

Central Florida average insurance costs by county (2026 estimates):

| County | Average Annual Premium | Typical Hurricane Deductible |

|---|---|---|

| Orange County | $2,800 to $3,400 | 2% to 5% of dwelling coverage |

| Brevard County | $2,600 to $3,200 | 2% to 5% of dwelling coverage |

| Volusia County | $2,330 to $2,900 | 2% to 5% of dwelling coverage |

Wind mitigation features significantly reduce your premiums. Installing hurricane straps, impact-resistant windows, and secondary water resistance can lower costs by 10% to 45%. Hip roofs fare better than gable roofs in hurricanes and qualify for additional discounts. A wind mitigation inspection documenting these features costs $75 to $150 but often saves hundreds annually on premiums.

Roof age and material directly impact your costs. Newer roofs with impact-resistant shingles receive better rates than older roofs with standard materials. Some insurers offer premium credits for roofs less than 10 years old or constructed with specific materials rated for high wind resistance.

Factors affecting your roofing insurance costs:

- Distance from coastline and elevation

- Roof age, material, and shape

- Wind mitigation features installed

- Claims history in your area

- Home’s overall condition and value

Pro Tip: Request roofing estimates before filing claims to compare repair costs against your deductible. If repairs cost $4,000 and your hurricane deductible is $6,000, filing a claim makes no financial sense and adds a claim to your record that could increase future premiums.

Understanding these costs helps you budget appropriately for potential roof damage. Many homeowners set aside emergency funds equal to their hurricane deductible to avoid financial stress when storms hit. This preparation ensures you can quickly authorize repairs without waiting for insurance payments or scrambling for financing.

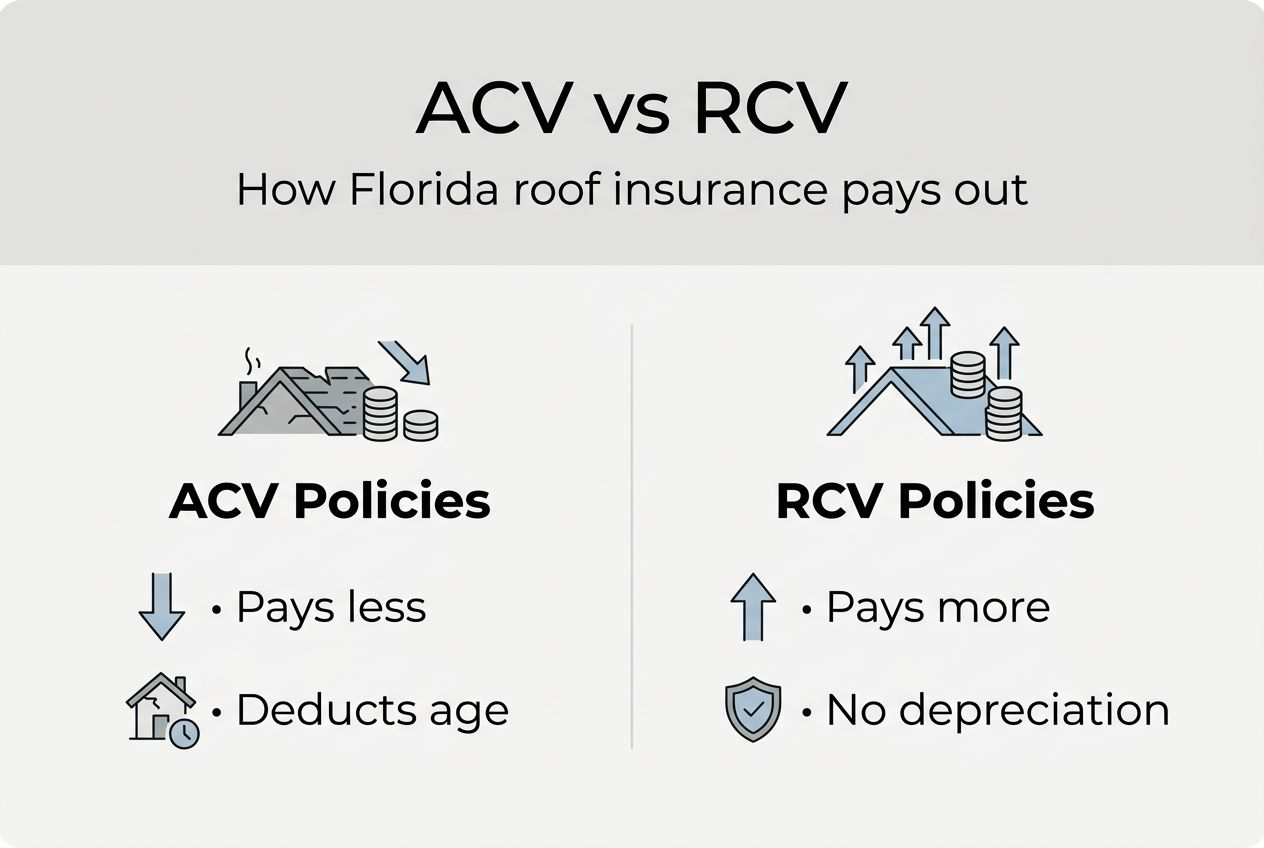

Types of roofing insurance coverage: ACV vs RCV

Your policy’s coverage type determines how much money you receive after roof damage. Actual Cash Value and Replacement Cost Value represent fundamentally different approaches to calculating claim payouts. Understanding this difference prevents surprises when you file claims.

Actual Cash Value coverage pays for repairs minus depreciation based on your roof’s age and condition. If your 15-year-old roof suffers storm damage, the insurer calculates what the damaged portion was worth in its depreciated state, not what replacement costs. This often leaves substantial gaps between insurance payments and actual repair bills.

Replacement Cost Value coverage pays the full cost to repair or replace damaged portions without deducting depreciation. If storm damage requires $12,000 in repairs, RCV coverage pays the full amount after you meet your deductible. This coverage costs more in premiums but provides significantly better protection, especially for older roofs or expensive materials.

ACV vs RCV coverage comparison:

| Coverage Type | Payout Calculation | Out-of-Pocket Cost | Best For |

|---|---|---|---|

| Actual Cash Value | Repair cost minus depreciation | Higher, covers depreciation gap | Older homes, tight budgets |

| Replacement Cost Value | Full repair cost, no depreciation | Lower, just deductible | Newer roofs, comprehensive protection |

The depreciation calculation under ACV policies follows industry standards based on roof age and expected lifespan. Asphalt shingle roofs typically last 20-25 years in Florida. A 10-year-old roof has lost roughly 40-50% of its value through depreciation. If repairs cost $10,000, ACV coverage might pay only $5,000 to $6,000, leaving you to cover $4,000 to $5,000 plus your deductible.

RCV policies sometimes use a two-payment structure. The insurer pays ACV initially, then releases the depreciation amount after you complete repairs and submit proof. This protects insurers from paying for repairs homeowners never complete while ensuring you receive full replacement value when you actually fix the damage.

Some policies offer endorsements to upgrade from ACV to RCV coverage for an additional premium. This upgrade makes sense for roofs over 10 years old or homes with expensive roofing materials like tile or metal. The extra premium cost often proves worthwhile compared to potential out-of-pocket expenses after major storm damage.

Key coverage considerations:

- Check your policy declarations page for coverage type

- RCV typically costs 10% to 20% more in premiums

- Depreciation schedules vary by roofing material

- Some insurers require RCV for roof replacement coverage

Policy endorsements can modify standard coverage terms. Roof surface endorsements may limit coverage to ACV for roofs over certain ages, even if your dwelling has RCV coverage. Reading your policy carefully and asking your agent specific questions about roof coverage prevents misunderstandings when you need to file claims.

Understanding your coverage type helps set realistic expectations for claim payouts. If you have ACV coverage on an older roof, budget for significant out-of-pocket costs beyond your deductible. This knowledge allows you to plan financially or consider upgrading your coverage before storm season arrives.

Navigating Florida’s 2026 roof insurance regulations and claims tips

Florida’s evolving insurance regulations directly impact your roof coverage. The 2026 roof regulations including the 15-Year Roof Rule allow insurers to require inspections for roofs over 15 years old but prohibit denying coverage based solely on age. This law protects homeowners from arbitrary coverage denials while giving insurers tools to assess actual roof condition.

Insurers can require you to repair or replace roofs showing significant wear before renewing your policy. If an inspection reveals missing shingles, extensive granule loss, or structural damage, the insurer may mandate repairs within a specific timeframe. Completing these repairs maintains your coverage, while ignoring them can lead to non-renewal.

Claim denial rates remain high due to pre-existing conditions, improper maintenance, and policy exclusions. Understanding common denial reasons helps you avoid these pitfalls. Insurers frequently deny claims when damage existed before the covered event, when homeowners neglected obvious maintenance needs, or when the damage falls under policy exclusions.

Steps to improve your claim success:

- Document your roof’s condition before storm season with photos and professional inspection reports

- Report damage immediately after storms, typically within 24-48 hours per policy requirements

- Take extensive photos and videos of all damage from multiple angles before making temporary repairs

- Mitigate further damage with tarps or emergency repairs, keeping all receipts

- Provide maintenance records and previous inspection reports to prove proper upkeep

- Communicate facts clearly without speculating about damage causes or admitting pre-existing problems

Timely reporting matters more than many homeowners realize. Most policies require prompt notification of damage, and delays can jeopardize your claim. Contact your insurer as soon as safely possible after a storm, even if you cannot fully assess damage immediately. This notification starts your claim timeline and documents when damage occurred.

Pro Tip: Schedule roof inspections annually and after every major storm. These inspections create a documented timeline of your roof’s condition, making it nearly impossible for insurers to claim damage was pre-existing when you have recent inspection reports showing your roof was sound.

Maintenance documentation serves as your primary defense against claim denials. Keep a file with all roof-related invoices, inspection reports, repair receipts, and correspondence with contractors. When an adjuster questions whether damage was pre-existing, this documentation proves your roof was properly maintained and damage resulted from the covered event.

“Proper documentation and timely reporting are the difference between successful claims and frustrating denials. Homeowners who maintain detailed records and act quickly after storms see significantly higher approval rates.”

Understanding policy exclusions prevents surprises during claims. Most policies exclude damage from settling, foundation issues, or design defects. If your roof leaks because flashing was improperly installed years ago, that constitutes a design or installation defect, not covered storm damage. Only damage directly caused by covered perils qualifies for claims.

Working with experienced roofing contractors who understand insurance requirements streamlines the claims process. Professional contractors document damage thoroughly, provide detailed estimates matching insurance industry standards, and communicate effectively with adjusters. Their expertise helps ensure you receive fair claim settlements covering all necessary repairs.

Protect your Central Florida home with trusted roof repair and installation

Understanding roofing insurance gives you the knowledge to protect your investment, but professional roofing services turn that knowledge into action. When storm damage strikes or your roof needs replacement, working with experienced contractors ensures repairs meet insurance requirements and local building codes.

Thomas Roofing and Repair provides comprehensive roof replacement and emergency repair services throughout Central Florida’s Brevard, Volusia, and Orange counties. Their team understands insurance claim processes and documents damage in ways that maximize your claim potential.

Professional inspections before and after storms create the documentation insurers require for successful claims. Thomas Roofing’s certified inspectors identify problems early, provide detailed reports, and work directly with insurance adjusters when needed. Their roofing guarantees give you confidence that repairs will last and meet all warranty requirements.

Contact Thomas Roofing and Repair for inspections, storm damage assessments, or roof replacements backed by solid craftsmanship and local expertise.

Frequently asked questions

What does roofing insurance typically cover in Florida?

Roofing insurance covers sudden damage from covered perils like hurricanes, wind, hail, and falling trees during storms. It does not cover gradual wear, maintenance neglect, or flood damage, which requires separate flood insurance.

How much are hurricane deductibles in Central Florida?

Hurricane deductibles typically range from 1% to 5% of your home’s insured value, meaning a $300,000 home could have deductibles between $3,000 and $15,000. These apply when named storms cause damage, separate from your standard deductible.

Should I choose ACV or RCV coverage for my roof?

Replacement Cost Value coverage is usually better because it pays full repair costs without depreciation deductions. Actual Cash Value coverage costs less but leaves you paying the depreciation gap, which can be substantial on older roofs.

What is Florida’s 15-year roof rule?

Florida’s 2026 regulations allow insurers to inspect roofs over 15 years old and require repairs if needed, but insurers cannot deny coverage based solely on roof age. Proper maintenance and documented condition matter more than age alone.

How can I prevent my roof insurance claim from being denied?

Document your roof’s condition with regular professional inspections, report damage immediately after storms, take extensive photos, keep all maintenance records, and work with experienced contractors who understand insurance requirements and documentation standards.

Recommended

- Roof Replacement Coverage: What Central Florida Owners Need

- Why invest in certified roofing in Central Florida 2026

- Central Florida roofing code requirements 2026: 130 mph standard

- Roof Replacement in Central Florida – What Homeowners Need to Know

- Roofing Company Orlando, FL

- Roofing Company Titusville, FL

- Roofing Company DeLand, FL