TL;DR:

- Roof type impacts insurance, inspection outcomes, and long-term savings more than resale percentage.

- Metal and tile roofs offer higher overall value through insurance discounts and red flag elimination.

- Consider ownership timeline, neighborhood preferences, and insurance benefits when choosing a roofing material.

Most homeowners expect a brand-new roof to pay for itself at the closing table. The reality is more complicated. Across U.S. home sales, the average recoup rate for a roof replacement sits around 52% of the total replacement cost. That number surprises a lot of people, and it tells only part of the story. The type of roof you install matters just as much as whether you replace it at all. In Central Florida’s stormy, insurance-complicated real estate market, choosing the wrong material can quietly cost you thousands, while the right choice pays dividends long before you ever list the home.

Table of Contents

- Why roof type matters more than you think

- Central Florida’s most common roof types: cost, resale, and ROI explained

- Beyond resale: How roof type affects insurance and inspection outcomes

- Maximizing ROI: Framework for Central Florida homeowners

- The uncomfortable truth about roof ROI most experts don’t mention

- Ready to choose the right roof for maximum ROI?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Roof type affects ROI | The material you choose directly impacts resale value, insurance, and buyer demand. |

| Metal and tile add hidden value | These higher-cost roofs may recover more through insurance savings and faster sales even if percentage ROI seems lower. |

| Effective ROI includes more than price | Factor in avoided concessions, insurance discounts, and how easily your home sells in Central Florida’s market. |

| Quality documentation boosts value | A well-documented roof upgrade increases buyer confidence and marketability during resale. |

Why roof type matters more than you think

When buyers walk through a home in Brevard, Volusia, or Orange County, they’re thinking about hurricanes, insurance premiums, and whether their lender will even approve the purchase. Your roof sits directly at the center of every one of those concerns. The specific material you choose shapes buyer psychology, insurance eligibility, and the outcome of every home inspection. That’s why roof type carries outsized weight in this market compared to many other parts of the country.

According to Opendoor’s roof value report, ROI differences by roof type are driven by three forces: how much buyers discount a home for roof age or poor condition, how much insurance and financing friction the roof creates, and how well the roof performs under wind and impact stress. In Florida, all three of those forces hit harder than anywhere else in the country.

Here’s what’s actually at stake when a buyer or their agent pulls up the listing:

- Roof age and condition directly influence whether an insurer will write a new policy on the home

- Roofing material affects which wind mitigation credits are available, often worth hundreds of dollars per year in premium reductions

- Inspection findings tied to roof condition frequently lead to buyer credit requests, delayed closings, or outright deal collapses

- Lender appraisers may flag roofs with fewer than three years of remaining useful life, limiting financing options for buyers

Making smart roofing choices isn’t just about what looks good in the neighborhood. It’s about understanding that your roof is doing financial work every single day you own the home, not just when you sell it.

“A roof that causes no problems is invisible to buyers. A roof that raises red flags is all they can see.” This is the principle that drives smart roof investment decisions in the Florida market.

There’s also what experts call “avoided cost ROI.” This is the money you never lose because your roof didn’t cause a problem. Think about the seller who avoids a $12,000 buyer credit request because their roof passed inspection. Or the homeowner who saves $1,800 per year on insurance premiums because their metal roof earned maximum wind mitigation credits. Those savings are real ROI, even though they never appear on a simple recoup percentage chart.

To maximize property value in Central Florida, you need to think about roofing ROI as a two-part equation: the value added at the point of sale, plus the accumulated savings and frictions avoided during the time you own the home.

Pro Tip: Keep every document related to your roof in a dedicated folder, including installation permits, warranty certificates, and wind mitigation inspection reports. Handing this packet to a buyer’s agent at the showing signals quality and often eliminates roof-related negotiation points entirely.

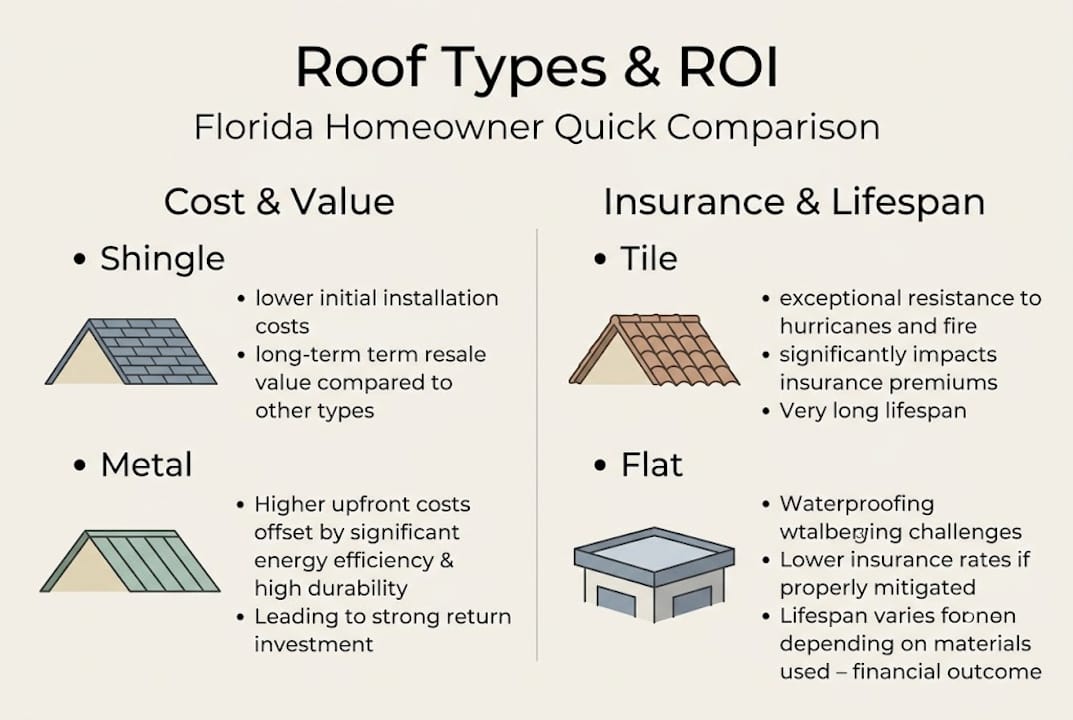

Central Florida’s most common roof types: cost, resale, and ROI explained

Understanding why roof type matters, let’s break down the specifics of Central Florida’s most popular options and see how they stack up in actual dollar terms.

Here’s a head-to-head comparison of the three most common roof types installed across Orange, Brevard, and Volusia counties:

| Roof type | Avg. installed cost (FL) | Typical lifespan | Approx. resale ROI % | Key insurance benefit |

|---|---|---|---|---|

| Asphalt shingle | $8,000 to $15,000 | 15 to 25 years | 61% to 68% | Standard coverage, limited wind credits |

| Metal (standing seam) | $18,000 to $35,000 | 40 to 70 years | 60% to 85%+ | Significant wind mitigation discounts |

| Concrete or clay tile | $20,000 to $40,000 | 30 to 50+ years | 55% to 75% | Strong wind resistance, hail resistance varies |

Redfin’s roof ROI data shows the national average sits near 52%, but metal and tile roofs in Florida are consistently positioned as higher-value systems that outperform basic asphalt when you account for total ownership benefit, not just the percentage of cost recouped at closing.

Let’s walk through three realistic scenarios for Central Florida homeowners:

- Asphalt shingle replacement at $12,000 with a 65% recoup rate returns roughly $7,800 in added resale value. Lower upfront cost, faster payback percentage, but shorter lifespan and fewer insurance perks.

- Metal roof installation at $28,000 with a 75% effective recoup rate (including insurance savings factored in over five years) returns roughly $21,000 in combined value. The percentage looks similar but the raw dollar return is dramatically larger.

- Tile roof installation at $32,000 with a 65% recoup rate still returns over $20,000 in value at sale, plus the visual premium tile commands in certain Central Florida neighborhoods, particularly in established communities in Orange County.

Key stat: Metal roofs in Florida can reduce annual homeowners insurance premiums by 20% to 30% depending on the insurer and the wind mitigation rating. Over a 10-year ownership period, that premium reduction alone could offset $10,000 to $20,000 of the higher installation cost.

Choosing the right roof material choices starts with knowing what your specific neighborhood, buyer pool, and insurance environment will reward. Your roof replacement guide should reflect local realities, not national averages.

Beyond resale: How roof type affects insurance and inspection outcomes

Now that we’ve compared roof types head-to-head, it’s vital to see how insurance and inspection realities amplify or shrink your ROI.

Florida’s insurance market is unlike any other state. Carriers have become extremely selective about which roofs they will insure, and the material and age of your roof directly affect whether you can get coverage, what you’ll pay for it, and how quickly a buyer’s insurer will approve a new policy at closing.

Here’s how major roof materials compare on insurance and inspection performance:

| Roof material | Insurance risk tier | Common wind mitigation credit | Typical inspection outcome |

|---|---|---|---|

| Asphalt (3-tab, aging) | High risk after 15 years | Minimal to none | Often flagged for replacement |

| Asphalt (architectural, new) | Standard | Low to moderate | Passes with documentation |

| Metal (standing seam) | Low risk | High: often 20% to 30% premium reduction | Passes readily, favored by insurers |

| Concrete or clay tile | Low to moderate | Moderate to high | Passes well when installed correctly |

The wind/impact performance of your roof material directly determines what credits you unlock and what problems you avoid at inspection. This is the connection most homeowners don’t see clearly until they’re sitting at the closing table watching a deal unravel.

Here’s what poor roof performance costs you in real terms:

- A buyer’s inspector flags an aging asphalt roof, and the buyer submits a $10,000 credit request

- Your insurance company refuses to renew your policy because your roof is over 20 years old, which spooks the buyer’s lender

- A buyer’s insurer quotes a premium so high for your older shingle roof that the buyer walks from the deal

- You lose your preferred listing price and accept a lowball offer just to close before the next storm season

Understanding roofing insurance in Florida is not optional for Central Florida homeowners. It’s a core part of your financial plan. Learning how roof inspection benefits your transaction can mean the difference between a smooth closing and a painful renegotiation.

Pro Tip: After installing a new metal or tile roof, immediately schedule an official wind mitigation inspection through a Florida-licensed inspector. The resulting report can be submitted to your insurance company within days, often triggering a premium reduction that starts showing up on your next renewal.

Maximizing ROI: Framework for Central Florida homeowners

After seeing how insurance, inspections, and the market play into your roof’s payoff, let’s lay out a practical framework to get the best results from your investment.

Most homeowners make the mistake of treating ROI as a single number: cost of roof divided by increase in sale price. That’s incomplete. The smarter approach is to treat total ROI as value added at sale plus all avoided costs accumulated during ownership. This complete ROI methodology shifts how you evaluate every option on the table.

Here’s a step-by-step framework built for Central Florida homeowners:

- Calculate your expected ownership timeline. If you’re staying 10+ years, the long lifespan and insurance benefits of metal or tile shift the math heavily in their favor. If you’re selling within three years, the higher upfront cost of premium materials may not fully recoup at closing.

- Get a wind mitigation assessment before choosing materials. Different roof shapes, decking types, and attachment methods qualify for different credits. A pre-installation consult with a qualified inspector tells you exactly what your new roof needs to earn maximum insurance savings.

- Research your buyer pool. Tile roofs command premiums in certain established Orange County neighborhoods but may be uncommon and therefore unrewarded in other parts of Brevard County. Match your material to what local buyers actually value.

- Price out the insurance difference. Call your insurer or broker and ask them to quote your current policy under three scenarios: existing roof, new architectural shingle, and new metal or tile. The dollar difference will tell you more than any ROI percentage.

- Document everything from day one. Permits, warranty cards, manufacturer specs, inspector reports, and wind mitigation certificates should all be organized and ready to hand over to a future buyer.

The major hidden ROI factors that often get overlooked include:

- Faster sale speed (a move-in-ready roof with documentation closes weeks faster on average)

- Elimination of buyer credit negotiations

- Annual insurance premium savings compounded over the ownership period

- Reduced maintenance costs, especially for metal roofs that may not need any significant attention for 30+ years

- Warranty transferability, which serves as a strong selling point

Considering roof replacement vs repair is also part of this framework. Sometimes a targeted repair makes financial sense. Other times, a full replacement is the only move that eliminates inspection risk entirely. Getting roofing estimates in Orlando from a qualified local contractor gives you accurate numbers to plug into your own calculations.

If the upfront cost feels challenging, roof financing options can spread the investment without delaying the upgrade. Working with affordable roofing contractors who understand Florida’s market also helps you avoid overpaying for materials or labor.

Pro Tip: Adjust your roof material choice based on how long you expect to live in the home and what the dominant home style is in your neighborhood. A metal roof on a street lined with tile homes might look out of place, while that same metal roof in a newer subdivision could be a strong differentiator.

The uncomfortable truth about roof ROI most experts don’t mention

Here’s something we’ve seen play out repeatedly across Central Florida: homeowners who choose premium roofing materials sometimes feel shortchanged when they look up their recoup percentage and see a number that’s lower than what their neighbor got with a basic asphalt shingle. The tables and percentages can genuinely mislead you.

The truth is that higher-cost roof types like metal and tile may show a lower percentage recoup than asphalt in some market segments. But percentage recoup is not the full story. It completely ignores the insurance savings, the inspection frictions avoided, the faster closings, and the years of reduced maintenance costs. A homeowner with a metal roof who saves $1,500 per year on insurance over 10 years has effectively earned back $15,000 that will never show up in a resale ROI calculation.

We also see too many homeowners get fixated on one number and ignore the real win: eliminating every red flag that buyers, lenders, and insurers use to chip away at your property value. A roof that no one has to worry about is worth more than any percentage can capture.

The best move is to look at roofing materials for Florida homes through the lens of your own timeline, risk tolerance, and financial goals. A roof that gives you peace of mind, keeps insurance affordable, and sails through every inspection is outperforming any alternative, even if the recoup percentage looks modest on paper.

Ready to choose the right roof for maximum ROI?

Choosing the right roof material in Central Florida is not a decision you should make from a single chart or a national average. Local conditions, insurance market realities, and neighborhood buyer expectations all shape which choice actually pays off for your specific property.

At Thomas Roofing and Repair, we work with homeowners across Brevard, Volusia, and Orange County every day to match the right roofing solution to their real financial goals. Whether you’re weighing a replacement, planning for a future sale, or need a professional inspection to understand where your current roof stands, we can help. Get started with roof installation in Horizon West, explore your roof replacement in Central Florida options, or schedule your Central Florida roof inspection today. Contact us for a free estimate and let’s make your roof work for you.

Frequently asked questions

Which roof type delivers the highest resale value in Central Florida?

Asphalt roofs typically show the highest resale ROI percentage, with recoup rates around 61% to 68%, but metal and tile often deliver greater long-term total value by reducing insurance costs and eliminating inspection red flags that eat into your net proceeds.

Does a new roof always increase my property value?

A new roof rarely pays back 100% of its cost at sale, but homeowners recoup roughly 52% of the replacement cost on average while also preventing buyers from requesting credits or discounts that would otherwise reduce your net sale price.

How does roof type impact my homeowners insurance in Florida?

Metal and tile roofs frequently earn significant premium discounts because their wind and impact performance qualifies for better wind mitigation ratings, while aging asphalt roofs can trigger coverage denials or steep rate increases.

Is it worth upgrading to tile or metal if I might move in a few years?

If you’re planning to sell within a few years, higher-cost metal and tile roofs may not fully recoup their installation cost at closing, but they sharply reduce the risk of deal-killing inspection findings and insurance complications that can delay or derail your sale.