TL;DR:

- A roof insurance claim is a request for coverage of sudden roof damage caused by events like storms or hail. Proper documentation, timely reporting, and understanding your policy type are key to maximizing your payout. Avoid mistakes such as signing early agreements or missing adjuster inspections to ensure a fair settlement.

A roof insurance claim is a formal request submitted to your homeowner insurance provider to cover damage to your roof caused by sudden, accidental events such as storms, hail, wind, or fallen trees. The industry term is a “property damage claim,” and understanding how it works before you need it is the difference between a full payout and a frustrating denial. Roof damage accounts for 70%–90% of all storm-related insurance claims, making it the single most common reason homeowners contact their insurer. Your policy type, deductible structure, and documentation quality all determine how much money you actually receive.

What is a roof insurance claim and what does it cover?

A roof insurance claim covers sudden, accidental damage to your roof from named perils listed in your homeowner policy. Standard covered perils include wind, hail, lightning, and falling trees or debris. Gradual deterioration, poor maintenance, and age-related wear are almost never covered. Knowing this distinction protects you from filing a claim that will be denied outright.

Most standard homeowner policies cover the roof structure, underlayment, flashing, gutters, and any interior damage caused directly by the roof breach. Coverage does not extend to cosmetic damage alone in many states, meaning dented but functional shingles may not qualify. The scope of what your policy covers depends on whether you carry an open-perils or named-perils policy. Open-perils policies cover all damage except what is explicitly excluded, while named-perils policies cover only what is listed.

Pro Tip: Read your declarations page before a storm hits. It lists your coverage type, deductible, and any roof-specific exclusions in plain language.

How does the roof insurance claim process work?

The roof damage insurance claim process follows a clear sequence. Skipping or rushing any step reduces your payout.

-

Report the damage to your insurer. Call your insurance company as soon as you discover damage. Carriers require filing within 30–60 days of the loss event. Missing this window is one of the most common reasons claims are denied.

-

Document everything before repairs begin. Photograph all visible damage from multiple angles. Save any debris, broken shingles, or fallen branches as physical evidence. A thorough roof damage documentation guide walks you through exactly what to capture and how to organize it.

-

Schedule the field adjuster inspection. Your insurer assigns a field adjuster who visits your property. Standard inspection timelines run 7–14 days from the claim filing date. Be present for this inspection. Walk the adjuster through every area of damage you documented.

-

Review the initial scope of loss. The adjuster produces a written scope of loss listing every damaged item and its estimated repair cost. This first estimate is almost always incomplete. Hidden damage, code upgrade requirements, and overlooked materials are routinely missing from the initial scope.

-

Work with a contractor on supplements. A qualified roofing contractor reviews the scope and submits supplement requests for missing items. Properly formatted supplements recover an average of $7,000 more per claim. This step alone is why choosing the right contractor matters as much as choosing the right insurer.

-

Receive payment in stages. Most carriers issue an Actual Cash Value advance first. After repairs are complete, the insurer releases the recoverable depreciation if you carry a Replacement Cost Value policy.

Pro Tip: Attend the adjuster inspection yourself and bring your own photos. Adjusters cover many properties quickly and can miss damage that is visible only from certain angles.

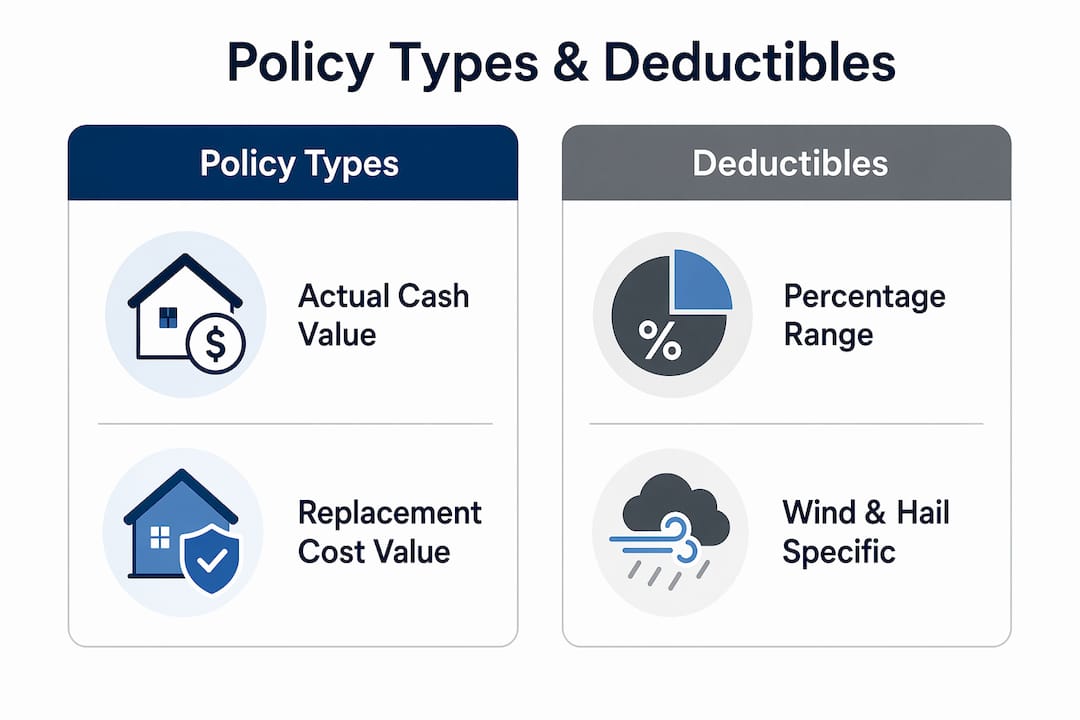

What policy terms affect your roof claim payout?

Two policy types determine how much money you receive: Actual Cash Value and Replacement Cost Value. ACV policies pay the depreciated value of your roof based on its age and condition at the time of loss. RCV policies pay the full cost to replace the roof with like materials, minus your deductible. A 15-year-old roof under an ACV policy may receive a fraction of what a new roof costs, leaving you with a significant gap to cover out of pocket.

| Policy type | How payout is calculated | Depreciation impact |

|---|---|---|

| Actual Cash Value (ACV) | Replacement cost minus depreciation | High. Older roofs receive much less. |

| Replacement Cost Value (RCV) | Full replacement cost minus deductible | Low. Depreciation is recoverable after repairs. |

Your deductible is the second major factor. Wind and hail deductibles typically range from 1%–5% of your dwelling coverage amount. On a $400,000 home with a 2% wind deductible, you owe $8,000 before insurance pays a dollar. That number changes the math on whether filing makes sense for smaller repairs.

Pro Tip: Calculate your deductible before you call your insurer. If the repair estimate is close to or below your deductible, filing may cost you more in future premiums than it saves today.

When should you file a claim vs. pay out of pocket?

Filing a roof insurance claim is the right move in some situations and the wrong move in others. The decision depends on damage severity, your deductible, and your claims history.

File a claim when:

- Storm damage is extensive and the repair cost clearly exceeds your deductible by a meaningful margin

- A single identifiable weather event caused the damage and you can document the date

- You have a clean or minimal claims history and the premium risk is low

- Structural integrity is compromised and delaying repairs would cause further interior damage

Pay out of pocket when:

- The repair cost is close to or below your deductible

- The damage is minor and cosmetic rather than structural

- You have filed another claim within the past three years

- Your insurer operates in a market where non-renewal risk is elevated

Filing a claim stays on your CLUE database record for five to seven years. CLUE stands for Comprehensive Loss Underwriting Exchange, and every insurer checks it when you renew or switch policies. Minor claims can trigger annual premium increases of $200–$400 for several years and raise the risk of non-renewal. That long-term cost often exceeds the payout on a small claim.

The storm damage repair cost guide from Thomasroofingandrepair breaks down typical repair costs by damage type, which helps you run this calculation before you call your insurer.

What are the most common roof claim mistakes to avoid?

Most homeowners underestimate how much the claim process rewards preparation and active involvement. These are the mistakes that cost the most money.

-

Signing an Assignment of Benefits too early. An AOB transfers your legal right to the insurance settlement directly to a contractor. Signing an AOB before independent assessment means losing control of your own claim. Use a contingency agreement instead. It binds the contractor to your claim only after approval and keeps you in control.

-

Skipping the adjuster inspection. Homeowner presence during the adjuster inspection reduces underpayment risk significantly. Adjusters work fast. Your documentation and your presence fill in gaps they would otherwise miss.

-

Accepting the first settlement offer without review. The field adjuster assesses damage on site, but 90% of carriers use Xactimate software and a desk adjuster sets the final pricing. That desk adjuster never sees your roof. Supplements submitted in Xactimate format are the standard way to recover for code upgrades, hidden damage, and missing line items. PDF invoices from contractors are routinely downgraded by carriers.

-

Failing to document before cleanup. Once debris is removed and temporary repairs are made, physical evidence disappears. Photograph everything before touching it, including interior water damage, attic insulation, and any structural members affected.

-

Waiting too long to act. Water intrusion compounds quickly in Central Florida’s climate. The emergency roof repair workflow from Thomasroofingandrepair outlines the fastest path from storm event to protected structure.

Pro Tip: Ask your contractor whether they submit supplements using Xactimate. If they use PDF invoices only, you are likely leaving money on the table.

Key Takeaways

A roof insurance claim pays only what your policy, deductible, and documentation support. Preparation before the storm and active involvement during the process determine your final settlement.

| Point | Details |

|---|---|

| Know your policy type | ACV pays depreciated value; RCV pays full replacement cost minus your deductible. |

| File within the deadline | Most carriers require filing within 30–60 days of the damage event to avoid denial. |

| Calculate your deductible first | Wind and hail deductibles of 1%–5% can exceed repair costs on minor damage. |

| Attend the adjuster inspection | Your presence and documentation reduce the risk of underpayment on the initial scope. |

| Use supplements, not PDFs | Xactimate-formatted supplements recover an average of $7,000 more per claim than invoice-only submissions. |

What I’ve learned from watching homeowners navigate roof claims

The homeowners who get the best settlements are not the ones with the most damage. They are the ones who treated the claim like a project from day one. They read their policy before calling the insurer. They photographed everything before touching anything. They showed up for the adjuster inspection with organized documentation and asked questions.

The single most damaging mistake I see is the AOB signature. A contractor shows up the day after a storm, offers to “handle everything,” and hands over a form that transfers the entire claim. The homeowner signs it because they are stressed and want someone else to take over. That signature removes them from every decision that follows. Contingency agreements exist for exactly this reason. They protect the homeowner without removing the contractor’s incentive to do good work.

Supplements are also widely misunderstood. Most homeowners assume the first check is the final check. It rarely is. Code upgrades alone, such as required ice and water shield or updated ventilation standards, can add thousands to a legitimate claim when submitted correctly. The desk adjuster who sets your final payout never visited your roof. A well-formatted Xactimate supplement is the only way to communicate what the field adjuster missed.

My honest advice: treat your roof insurance policy the way you treat your car insurance. Know what it covers before you need it. The insurance claim documentation steps guide from Thomasroofingandrepair is worth reading now, not after the next storm.

— Results

Thomasroofingandrepair: your partner through every claim step

Storm damage in Central Florida moves fast. So does the window for filing a valid claim.

Thomasroofingandrepair provides professional roof inspection services to document damage accurately before your adjuster arrives, giving your claim the foundation it needs. The team handles storm damage repair, full roof replacement, and emergency response across Brevard, Volusia, and Orange counties. Every estimate is built to support your claim, not complicate it. If you need fast, reliable service after a storm, Thomasroofingandrepair offers emergency storm repair with the documentation workflow that insurers expect. Contact Thomasroofingandrepair for a free estimate and claim consultation today.

FAQ

What is a roof insurance claim exactly?

A roof insurance claim is a formal request to your homeowner insurer for payment to repair or replace roof damage caused by a covered peril such as wind, hail, or a fallen tree. It is the standard mechanism for recovering costs after sudden, accidental roof damage.

How long does the roof insurance claim process take?

The field adjuster typically inspects within 7–14 days of filing, and initial payment follows shortly after. Full settlement, including recoverable depreciation on RCV policies, is released after repairs are completed and documented.

What does roof insurance actually cover?

Standard homeowner policies cover sudden damage from named perils including wind, hail, lightning, and falling objects. Gradual wear, poor maintenance, and cosmetic-only damage are typically excluded from coverage.

Should I always file a claim for roof damage?

Not always. If the repair cost is close to your deductible, paying out of pocket avoids a CLUE record entry and potential premium increases of $200–$400 annually for several years.

What is the difference between ACV and RCV for roof claims?

ACV pays the depreciated value of your roof at the time of loss, while RCV pays the full replacement cost minus your deductible. RCV policies release the withheld depreciation after repairs are completed and verified.