TL;DR:

- Florida homeowners often underestimate the impact of high roofing deductibles, leading to unexpected costs.

- Hurricane deductibles apply statewide during storm warnings, regardless of actual storm impact location.

- Understanding deductible types and eligibility criteria helps homeowners avoid costly surprises after storm damage.

Most Central Florida homeowners assume their insurance policy fully covers roof damage after a storm. That assumption can cost thousands. A deductible is the amount you pay out of pocket before your insurance company contributes a single dollar to your claim. In Florida, those deductibles can be steep, especially after hurricanes, and the rules about what qualifies for coverage are more complex than most people realize. This guide breaks down exactly how roofing deductibles work, which expenses count, which do not, and what local homeowners in Brevard, Volusia, and Orange counties need to know before filing a claim.

Table of Contents

- What is a roofing deductible and how does it work?

- Types of roof deductibles: Hurricane vs all other perils

- What roof expenses are eligible—or not eligible—for deductible claims?

- Edge cases, special scenarios, and pitfalls for Central Florida homeowners

- The uncomfortable truth about roofing deductibles in Florida

- Have roofing deductible questions? Get expert support in Central Florida

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Deductibles vary by event type | Your out-of-pocket costs will depend on whether the damage was caused by a hurricane, storm, or other peril. |

| Not all expenses qualify | Only storm-related repair costs are eligible for deductible claims, not routine maintenance or cosmetic work. |

| Policy details matter | Roof age, claim size, and policy fine print can all affect how your deductible works and what is paid out. |

| Preparedness lowers risk | Understanding your deductible helps you budget and avoid surprises during Florida’s storm season. |

What is a roofing deductible and how does it work?

A deductible is not a penalty. It is simply your agreed share of the repair cost whenever you file a claim. Before your insurer writes a check, you are responsible for paying that portion directly. Understanding this foundational concept is what separates homeowners who navigate claims smoothly from those who are blindsided at the worst moment.

Florida policies typically use one of two deductible structures. The first is a flat dollar amount, such as $1,000 or $2,500. The second is a percentage of your home’s insured value, most commonly 2%. On a home insured for $250,000, a 2% deductible means $5,000 comes out of your pocket before insurance pays anything. That is a significant number, especially when storm season hits without warning.

Here is a quick comparison of common deductible structures:

| Deductible type | Example amount | Best for |

|---|---|---|

| Flat dollar | $1,000 to $2,500 | Predictable, fixed risk |

| 2% of insured value | $5,000 on $250K home | Lower annual premiums |

| 5% of insured value | $12,500 on $250K home | Significant premium savings |

Now here is where many homeowners make a costly mistake. Small claims below the deductible result in zero payment from your insurer. If your roof repair costs $1,800 but your deductible is $2,500, you are paying entirely out of pocket. Filing a claim anyway can raise your premium without any financial benefit.

Common deductible scenarios to understand:

- Minor leak repairs often cost less than your deductible

- Storm damage from a named hurricane triggers a separate, higher deductible

- Emergency patching after a wind event may or may not meet your threshold

- Flat-rate deductibles are easier to plan for than percentage-based ones

Pro Tip: Before filing any claim, get a professional estimate. If the repair cost is close to or below your deductible, it may be smarter to pay out of pocket and protect your claims history. You can learn more about the basics in this roofing insurance basics guide we put together for Florida homeowners.

Types of roof deductibles: Hurricane vs all other perils

Florida does not treat all storms equally, and neither do insurance policies. The type of storm that damages your roof determines which deductible kicks in, and the difference can be dramatic.

Hurricane deductibles apply specifically when a named hurricane is involved. These deductibles typically run from 2% to 5% of your home’s insured value. On a $300,000 home, that is $6,000 to $15,000 before insurance pays a cent. This is not a punishment. It reflects the catastrophic risk insurers take on in a state that sits directly in the path of Atlantic hurricanes.

Here is the detail that surprises most people: a hurricane deductible applies statewide the moment a hurricane watch or warning is issued anywhere in Florida. You do not need to live in the affected county. If a warning goes out for the Gulf Coast while you are in Brevard County on the Atlantic side, your hurricane deductible still applies to any damage you sustain.

All Other Perils (AOP) deductibles cover everything outside of a named hurricane. This includes tropical storms, wind events, hail, and standard weather damage. AOP deductibles are usually the flat dollar amounts, making them more predictable and generally lower than hurricane deductibles.

Comparison at a glance:

| Event type | Deductible triggered | Typical amount |

|---|---|---|

| Named hurricane | Hurricane deductible | 2% to 5% of insured value |

| Tropical storm | AOP or wind/hail deductible | $1,000 to $2,500 flat |

| Hail damage | AOP or wind/hail deductible | $1,000 to $2,500 flat |

| Standard wind | AOP deductible | $1,000 to $2,500 flat |

Knowing whether your damage qualifies as a hurricane event versus an AOP event directly affects how much you owe. Before deciding whether to repair or replace, review what type of event caused the damage. Our roof replacement vs repair resource walks through how to evaluate your options, and our Central Florida roof replacement guide covers local cost factors in detail.

What roof expenses are eligible—or not eligible—for deductible claims?

Understanding which deductible applies is just one step. The next is knowing exactly which expenses insurers will actually consider when processing your claim. Not everything that happens to your roof qualifies.

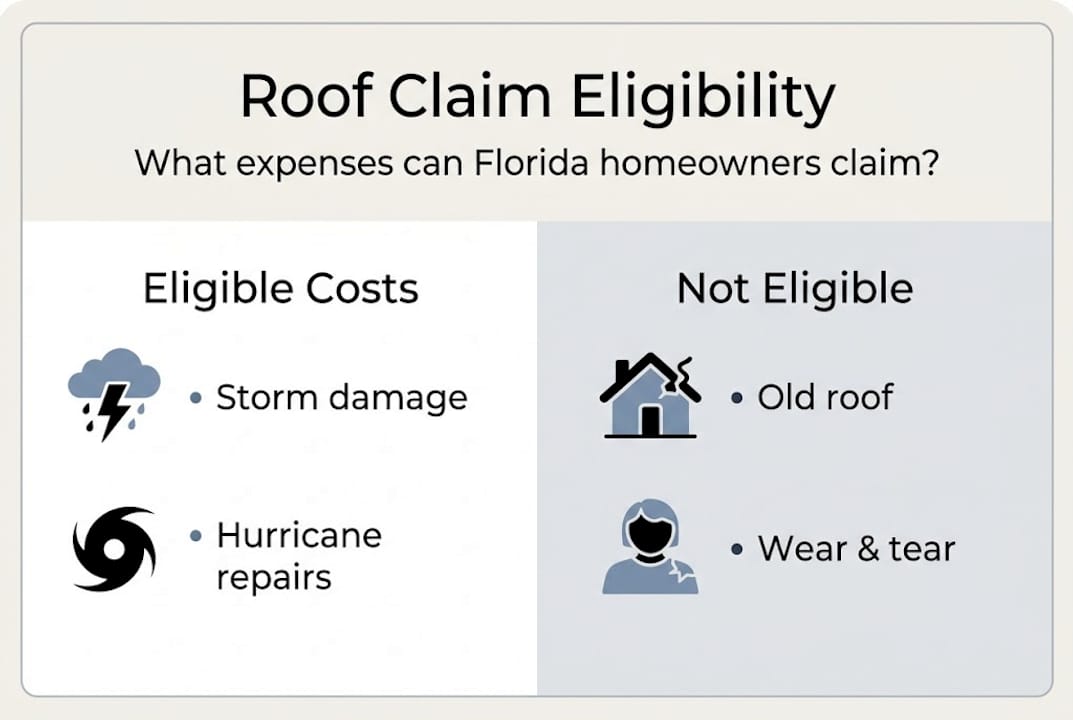

Eligible roofing expenses typically include:

- Roofing materials damaged by a covered storm event

- Labor costs for storm-related repairs or full replacement

- Damaged shingles, tiles, or metal panels caused by wind or hail

- Water barrier and underlayment replacement tied to storm damage

- Structural decking repairs if the damage stems from a covered peril

Non-eligible charges that insurers will reject:

- Routine maintenance such as resealing or recoating

- Cosmetic upgrades or improvements made during repairs

- Normal wear and tear over time

- Pre-existing damage that was never addressed

- Damage caused by neglect or lack of upkeep

One of the most overlooked issues in Florida is roof age. Roofs older than 15 years may face partial reimbursement or outright claim denial, even when the homeowner has paid the deductible in full. Insurers may apply depreciation so heavily that your actual payout is minimal. Some Florida policies for older roofs pay only actual cash value rather than replacement cost, which means you absorb the difference between what your roof is worth now and what a new one costs.

Before assuming your older roof is covered, review your policy language carefully. Look for terms like “actual cash value” versus “replacement cost value.” The gap between those two terms can easily run into the thousands. Knowing your roofing warranties and exclusions ahead of time gives you far better footing during the claims process. It is also worth getting a professional roofing estimate before speaking with your adjuster so you have solid numbers in hand.

Pro Tip: Keep a folder with dated maintenance invoices, inspection reports, and photos of your roof every year. If you ever need to prove your roof was in good condition before storm damage, this documentation can be the difference between a paid claim and a denied one.

Edge cases, special scenarios, and pitfalls for Central Florida homeowners

Knowing which expenses are deductible leads naturally to a review of special cases and pitfalls. Here is where Florida homeowners often get tripped up.

The most common mistake we see is filing a claim without knowing the repair cost first. If the damage is minor and the estimate comes in below your deductible, you get nothing from insurance but still have a claim on your record. That claim can raise your premium for years.

Another pitfall involves the statewide hurricane rule. Many homeowners in Central Florida believe that because their county was not in the storm’s direct path, they will use their standard AOP deductible. That is not how it works. Hurricane deductibles or AOP rules apply based on official watch and warning declarations, not local impact. A homeowner in Orange County can owe a full hurricane deductible even if the storm made landfall far away.

Some insurers offer optional roof deductibles that reduce your annual premium in exchange for higher out-of-pocket exposure during a claim. This can be a reasonable trade-off if you have savings set aside. It becomes a financial trap if you do not.

Common pitfalls to avoid:

- Assuming all storm damage is automatically covered

- Not reading the fine print on hurricane deductible triggers

- Failing to document damage with photos before any cleanup or tarping

- Skipping annual inspections that could catch issues before they become claims

- Choosing a lower premium without modeling the worst-case deductible scenario

“Preparedness is not just about storm shutters and evacuation routes. It is about understanding your financial exposure before the wind starts.”

Our roof repair tips for Florida homeowners and storm damage roof examples can help you identify what to document and when to act fast.

The uncomfortable truth about roofing deductibles in Florida

Here is what most insurance guides will not tell you plainly: the premium is not the number that matters most. The deductible is.

We work with Central Florida homeowners every storm season, and the pattern is consistent. The family that chose the cheapest policy is often the one calling us in a panic after a hurricane, stunned to learn they owe $10,000 before their insurer contributes anything. That is a real scenario, not a worst-case fantasy.

Low premiums feel like savings. High deductibles feel like punishment. The only way to close that gap is preparation. Build an emergency fund that matches your hurricane deductible, not just a few hundred dollars. Work with local roofers in Florida who understand how insurers in this state operate and can give you honest guidance on what damage qualifies and what it will cost. An informed homeowner asking the right questions before a storm is always better positioned than one reacting in the aftermath.

Have roofing deductible questions? Get expert support in Central Florida

Navigating roofing deductibles is genuinely complicated, and the stakes in Central Florida are high every storm season. You deserve straight answers before you make a claim decision that could affect your premium or leave you with unexpected costs.

At Thomas Roofing and Repair, we help homeowners across Brevard, Volusia, and Orange counties understand their options before and after damage occurs. Our storm damage repair guide walks through the full post-storm process, and our emergency roof repair workflow is available when you need answers fast. Reach out today for a free estimate and get the local expertise your roof depends on.

Frequently asked questions

What roofing expenses are typically not covered by my deductible?

Normal wear and tear, cosmetic improvements, and routine maintenance are not covered by your insurance deductible. Only storm-related damage from a covered peril qualifies.

How do hurricane deductibles work for all Central Florida homeowners?

A hurricane warning statewide activates the hurricane deductible for all Florida policyholders, regardless of where you live or how close the storm came.

Can I lower my insurance premium by choosing a higher roof deductible?

Yes, but optional roof deductibles for savings come with more out-of-pocket risk if you file a claim, so make sure your emergency fund can cover the difference.

What happens if my roof claim is less than my deductible?

Claims below deductible result in zero insurance payment. You are responsible for the full repair cost, and the claim may still affect your premium.

Does an old roof affect what I can claim for deductibles?

Yes. Roofs over 15 years may see limited coverage or outright claim denial, even after you have paid your full deductible amount.